By Paul Murray, CEO Life & Health Reinsurance, Swiss Re

SINGAPORE – Media OutReach Newswire – 9 July 2026 – Op-ed by Paul Murray, CEO Life & Health Reinsurance, Swiss Re.

Ten years.

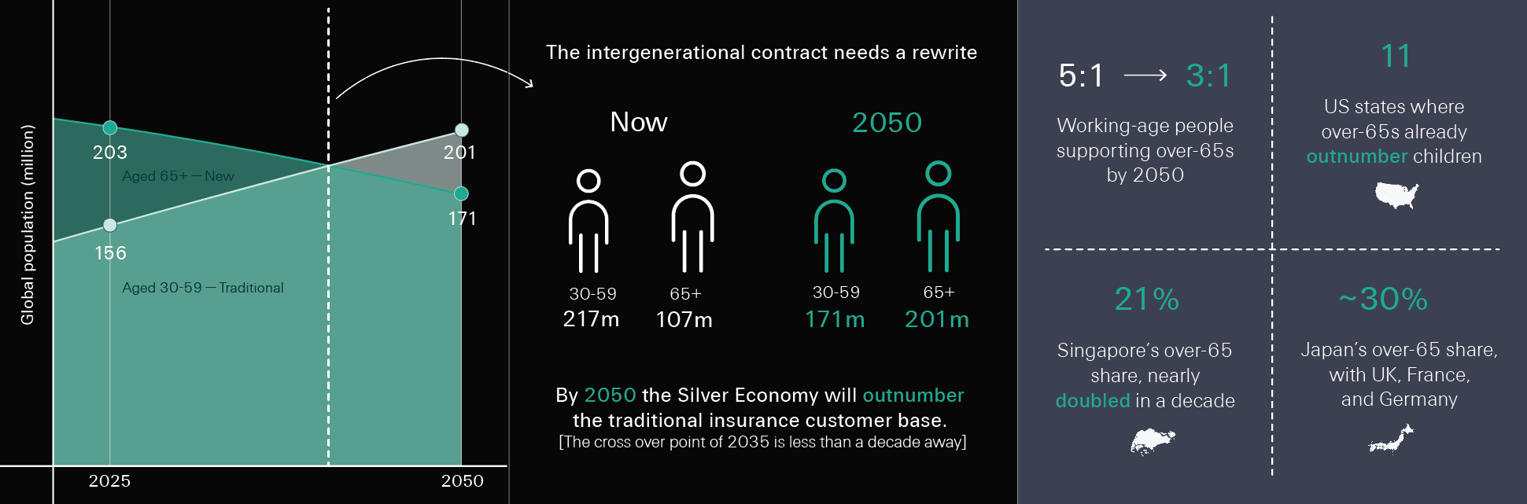

That is roughly how long we have before many societies reach one of the most defining demographic tipping points of our era: the point at which the “new” silver economy (over 65’s) outnumber people aged 30-59 who have traditionally been the bedrock of the life and pensions system.

The significance of this shift goes far beyond demographics.

It represents a symbolic moment that forces us to rethink the intergenerational contract: how we provide care and financial security for people as they move into later life – and how we finance a new set of needs.

The demographic evidence is already visible across major economies. In the US, adults aged 65 and over already outnumber children in 11 states. Singapore’s over-65 population has nearly doubled in a decade to 21%. Japan is approaching 30%. The UK, France and Germany are not far behind

These numbers are well-known. But their meaning is not yet fully reflected in our industry’s existing product strategy.

The tipping point is also more than a statistical curiosity. We will experience it through the decisions we make coming into retirement and to secure the future of the generation coming after us. We will need to make new choices on how we fund care. We will need to make new assumptions about when to retire. And we will face a new reality around how much of the financial burden falls on the state, families or the individual.

Families have always carried the weight of old age, even as pensions, healthcare systems and social care programmes have broadened that responsibility across society.

But the arithmetic underpinning the system is breaking. Globally, the ratio of working-age people financially supporting each person over 65 is projected to fall from around five-to-one in 2021 to three-to-one by 2050. Across developed markets, debates about pension reform, healthcare funding and retirement ages reflect the same underlying question: how do we maintain security and dignity later in life when there are fewer hands to carry the weight?

It’s not a crisis of demographics. It’s a crisis of design – our systems were built for shorter lives and larger workforces, and they haven’t been rebuilt for the world we are actually entering.

That insight matters because it challenges how we think about insurance’s role. I believe we have less than a decade to develop the products that the older consumers who make up the Silver Economy – and their families – will need.

There will be no silver bullet. We cannot return to a single solution based around family care versus public provision. The individual retiree will be the focus, but our thinking will need to be based on a more collaborative model in which families, governments, communities and the private sector work together.

Recent Swiss Re consumer research in France and Germany revealed something striking. People don’t think about later life in terms of pensions or insurance policies. They think about practical outcomes: staying independent, being resilient when health shocks hit, not becoming a burden to their children.

Our industry has spent decades optimising for wealth accumulation and income protection during working years. Ageing societies demand we apply the same rigour to what happens after.

That does not mean the intergenerational contract has failed. It means it is evolving.

We are already seeing what that evolution looks like in practice.

- Senior health products in Asia are closing a real gap —The median age of cancer diagnosis is 67, yet many critical illness policies expire before retirement even begins. The result is high out-of-pocket expenses, stressed public healthcare, and increased burden on families. With dedicated products to cover later life illnesses, such as senior cancer products we are effectively closing a protection gap.

- Long term care in France has had some success with private solutions alongside public provision. With over 1.4 million people covered by private long term care insurance, France has built a strong risk pool that directly addresses one of the strongest concerns expressed by consumers: not becoming a burden on the next generation.

- Deferred annuities offer a third path beyond the binary “draw-down versus annuity” thinking. By combining flexibility today with guaranteed income later, they help transform longevity from an individual financial risk into one that can be shared more broadly.

At first glance these solutions appear very different. In reality, they are pieces of the same puzzle. Each expands the circle of support around the individual. They help families carry less of the burden alone, and they complement the work of state safety nets.

That is what the next evolution of the intergenerational contract looks like in practice.

Ageing societies are one of humanity’s great achievements. But if our products and institutions stay built for a demographic reality that no longer exists, achievement curdles into liability.

We have a decade to close that gap. Let’s treat it as a product-development window, not a deadline.

Disclaimer

Certain statements and illustrations contained herein are forward-looking and are made for informational purposes only. These statements (including as to plans, objectives, targets, and trends) and illustrations provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to a historical fact or current fact. Readers are cautioned not to place undue reliance on forward-looking statements. Swiss Re undertakes no obligation to publicly revise or update any forward-looking statements, whether as a result of new information, future events or otherwise. Further information on forward looking statements and the use of information contained in this publication can be found in the Legal Notice section on Swiss Re’s website.

Hashtag: #SwissRe #lifeinsurance #reinsurance

![]() https://www.swissre.com/

https://www.swissre.com/![]() https://www.linkedin.com/company/swiss-re/

https://www.linkedin.com/company/swiss-re/

The issuer is solely responsible for the content of this announcement.

About Swiss Re

The Swiss Re Group is one of the world’s leading providers of reinsurance, insurance and other forms of insurance-based risk transfer, working to make the world more resilient. It anticipates and manages risk – from natural catastrophes to climate change, from ageing populations to cyber crime. The aim of the Swiss Re Group is to enable society to thrive and progress, creating new opportunities and solutions for its clients. Headquartered in Zurich, Switzerland, where it was founded in 1863, the Swiss Re Group operates through a network of around 70 offices globally.

{kind=link}