Let’s use the following example of a 1,500 sq ft fully furnished, two-bedroom, three-bathroom apartment in Mont Kiara valued at RM1 million, with rental at RM4,000 per month and a RM500 monthly management fee. We also assume that for 5 years, the property is perpetually rented. The rental yield is [(4000-500) x 12]/1,000,000 or 4.2%.

While this is simple enough math, it doesn’t take into account appreciating (or depreciating!) property. Nor does it take into account the upfront costs you probably paid to renovate the home for it to be competitively rented out. And what about those annual taxes? Or that one-month agent fee you paid?

Going over the variables for this exercise, we get:

(A) Initial outlay – including legal fees, down payment and booking fees = -RM150,000

(B) Monthly loan payments = -RM3,800

(C) Upfront renovation works = -RM50,000

(D) Monthly management fee = -RM500

(E) Monthly rental income = RM4000

(F) Taxes and property insurance = -RM1000

(G) Hypothetical net selling price of the property in year 5, minus RPGT and marketing/selling costs (eg. agency and lawyer fees) = RM1,100,000

(H) Hypothetical remainder of loan outstanding on the property in year 5 = RM790,000

Step 1: Calculate net inflow or outflow for each year

Let’s put the values below in Column B, next to the corresponding years in Column A.

Year 1 = A + (B x 12) + C + (D x 12) + (E x 11) + F (don’t forget the one month agency fee!)

Year 2 = (B x 12) + (D x 12) + (E x 12) + F

Year 3 = (B x 12) + (D x 12) + (E x 12) + F

Year 4 = (B x 12) + (D x 12) + (E x 12) + F

Year 5 = (B x 12) + (D x 12) + (E x 12) + F + G – H

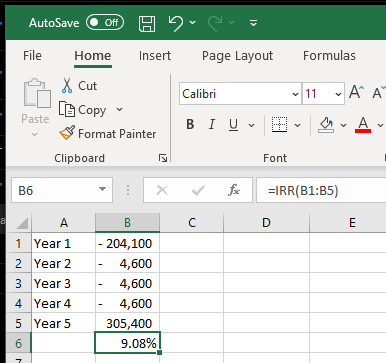

Step 2: Input the formula for IRR in Excel

In cell B6, input =IRR(B1:B5) to select the values of the cash movements in Step 1 above.

This should result in an IRR of 9.08%.

Summary

In short, the internal rate of return is an annualised investment return which is directly comparable to other asset class returns. For example, if a share at the end of one year gives you 14%, inclusive of capital gains of the stock as well as dividends, then this number becomes immediately comparable to the IRR of the property.

The trick here is to be realistic and be honest with yourself. After all, there’s no point cheating in comforting yourself that these property investments are “paying for themselves”. Using ratios and numbers such as IRR enables astute property investors to make logical decisions on what represents a good or not-so-good investment decision.

Click here to read the full article about how to spot property investment opportunities in Malaysia.

About the author

Rozanna Rashid is a Licensed Financial Planner (CFP, IFP) and holds an MSc in Real Estate Economics & Finance from the London School of Economics & Political Science. Her background is in corporate banking and Islamic finance and she can be contacted at rozanna@alpine-advisory.com.

{kind=link}