“Soo Yee, I can’t make any investments. I don’t have money left every month, how do I even invest?”

This is a common reply when I bring out the topic of investment. And no, you don’t really need a large amount of cash savings to start investing!

Did you know that you have the option to invest your EPF monies into EPF approved investments via the Member Investment Scheme (MIS)? Let me explain more below.

1. EPF Member Investment Scheme (MIS)

MIS was introduced back in November 1996 for EPF members to diversify, boost and strengthen their retirement savings.

In short, if you have enough funds in your EPF account 1, you can invest part of the funds into EPF approved investments via appointed fund management institutions (FMIs) including Unit Trust Management Companies and Asset Management Companies.

2. Advantages of MIS

a. Allows you to enhance investment returns

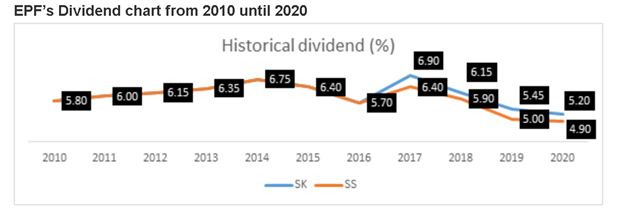

At the end of February 2021, EPF announced the 2020 dividend rate for Conventional accounts and Syariah accounts, paying out 5.2% and 4.9% respectively.

But what has the historical rate of EPF dividends looked like?

SK = Conventional AccountSS = Syariah AccountThe graph above is taken from the EPF website (as of 26 May 2021)

So while EPF has been paying a solid return each year, MIS provides the opportunity and potential for you to increase your investment returns and boost your retirement savings overall.

b. Enables you to increase exposure to foreign markets

Have you thought about where EPF decides to invest your money?

As at December 2020, EPF invested 67% of its investment assets in Malaysia and the remaining 33% outside Malaysia.

The numbers show that the majority of your EPF money is invested in Malaysia.

So if you’d like to have greater exposure to foreign markets, you can diversify your investments overseas via MIS.

c. Empowers you to have some control over your EPF investment

You can now choose to invest according to your risk profile.

There are EPF approved investment options for you to match your objectives and risk appetite.

3. Disadvantages of MIS

a. No guarantee of investment returns

For all its benefits, please note that any investment done via MIS doesn’t come with any guaranteed return, while EPF has a minimum guarantee of 2.5% dividend. You might get a higher or lower return compared to the EPF dividend rate, depending on your actual investment return.

You are solely responsible for the investment via MIS that you made.

b. Not entitled to EPF dividends

One of the big downsides is that the EPF money that you channel into MIS is no longer eligible for EPF dividends. Basically, you’re on your own. However, if you’re confident about your investment, this shouldn’t concern you.

c. MIS investments come with fees

Investment fees (such as sales charges, management fee and trustee fee) might eat up your investment returns. You must ensure that your investment returns (after deducting fees) will still be on par with EPF dividends at the very least.

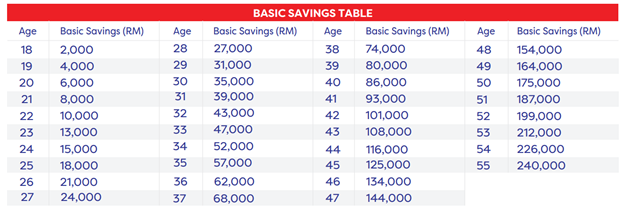

4. How much can you invest under MIS?

You may invest up to 30% of savings in excess of basic savings in account 1 with EPF. You may continue investing via MIS every three months as long as your balance in account 1 exceeds your required basic savings and fulfills all EPF requirements.

To confirm your eligible investment amount for MIS, you may check it under the i-akaun website.

Go to i-akaun website → withdrawal tab → withdrawal eligibility → member investment scheme.

The number that appears next to the member investment scheme is the amount eligible to invest via MIS.

Alternatively, you can also do a self-calculation of how much you can invest under MIS.

The formula is as below:

(EPF account 1 value – required basic saving in account 1 based on your age) x 30%Basic Saving Table from EPF website (as of 26 May 2021)

The minimum savings benchmark set by the EPF will be updated from time to time. You may check out the latest minimum savings required on the EPF website.

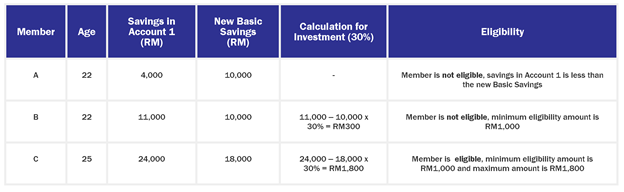

Sample calculation from EPF website (as of 26 May 2021)

5. Your investment options under MIS

You may invest via EPF in approved Unit Trust Management Companies and Asset Management Companies under MIS.

epf member investment scheme mis

Difference between investing into unit trust funds compared to managed account (portfolio of unit trust)

In summary, any investment that you may choose to do via MIS comes with pros and cons. Do research and understand all the risks that you’re taking before proceeding with investing. If you have further enquiries on EPF investment via MIS, I suggest that you seek out a financial professional to discuss and design an investment plan that matches both your risk profile and investment objectives.

About the author

Kuah Soo Yee is a Licensed Financial Planner (CFP) who is passionate about helping people make sound financial decisions and achieve their financial goals, and recently launched her own app. Her personalised strategies and advice have helped many to gain better clarity and take firm control of their financial future. She can be contacted at soo.yee@ipp.com.myWebsiteLinkedInFacebookInstagram

So while EPF has been paying a solid return each year, MIS provides the opportunity and potential for you to increase your investment returns and boost your retirement savings overall.

So while EPF has been paying a solid return each year, MIS provides the opportunity and potential for you to increase your investment returns and boost your retirement savings overall.

In summary, any investment that you may choose to do via MIS comes with pros and cons. Do research and understand all the risks that you’re taking before proceeding with investing. If you have further enquiries on EPF investment via MIS, I suggest that you seek out a financial professional to discuss and design an investment plan that matches both your risk profile and investment objectives.

In summary, any investment that you may choose to do via MIS comes with pros and cons. Do research and understand all the risks that you’re taking before proceeding with investing. If you have further enquiries on EPF investment via MIS, I suggest that you seek out a financial professional to discuss and design an investment plan that matches both your risk profile and investment objectives.

{kind=link}