This article is written to share some steps for you to consider when evaluating properties as an investment vehicle in Malaysia.

Think of it as a methodology for you to apply during your first round of scouting properties before going into more detailed research.

This selection process can be applied to property investment opportunities in both the primary market (properties under construction) and the secondary market, including auction properties.

The goal is to identify a suitable area and then select property that will represent a logical, financially-suited and tax-effective investment vehicle.

1. Look for established and planned infrastructure

One of the specific elements that influences demand within an area is the degree to which established and planned infrastructure is readily accessible to tenants.

Thus, it’s crucial that the existing and planned infrastructure surrounding property is critically identified and assessed.

Ask yourself why property in areas like Taman Tun Dr Ismail (TTDI), Mont Kiara, Bangsar and Desa Park City are very sought after?

One factor is that these neighbourhoods are matured, secure and self-sufficient townships that offer many modern conveniences — from good schools, access to banks, retail and F&B outlets, and many popular public parks.

Using TTDI as an example, it’s close to popular commercial developments such as 1Utama Shopping Centre, the Bandar Utama City Centre, and the Curve, as well as a number of multinational companies that base their offices nearby like Tesco and IKEA in Bandar Utama.

It also has a green lung of Lembah Kiara as a public park.

Infrastructure can be divided into two broad categories:

i) Accessibility – Local transportation links like access to local bus routes, MRT/LRT feeder buses, train stations, access to highways and also major arterial roads

ii) Local amenities – schools (including international/private schools), shopping centres, parks, hospitals, recreational areas, jogging/cycling paths, public parks etc

An attractive area for property investment is an area with amenities and rich infrastructure, of which there are several in Malaysia.

Alternatively, you could also look at areas that have some upcoming planned infrastructures like new highways (DASH, SUKE), highway access (MEX extension or interchange add ons), new MRT lines, LRT lines, and convenient access to commercial areas with eateries, banks and offices.

Other key indicators include sustainable malls (not just any mall, but those with established management with experience running malls that are well occupied/tenanted and well patronised), government or private/international schools, universities, public transportation, green lungs like parks and recreational areas, and working populations with a heavy focus on professionals in the middle to high-income group.

However, the time it would take for these infrastructures to be resident-accessible is a factor that shouldn’t be ignored.

Remember that you have to take into account the duration for your own target property to be built as well as the maturity of new infrastructures (highway, MRT, LRT, new central business district, malls etc) to be ready.

The faster one expects infrastructure to materialise, the quicker and better the chance of a property investment yielding capital appreciation while simultaneously lowering the risk of the infrastructure project being postponed or worse still, called off entirely.

Many will testify that this is not an uncommon occurrence in Malaysia!

2. Observe the residential vacancy rate and supply of similar properties

The same fundamental economic forces that affect the share market or even the price of coffee in your neighbourhood cafe are the exact same forces that affect the price and rental of the property market: supply and demand.

Naturally, an area with high demand but limited supply will inevitably experience above-average capital growth. An area that is “oversupplied” in contrast to demand will result in lower average capital growth.

A property investor in an oversupplied market may be forced to:

i) experience an extended vacancy period;

ii) be forced to revise the rental rate downwards to attract a potential tenant in a competitive market environment; or

iii) incur a greater than anticipated cash outflow/expense as a result of lower rental yield and/or extended vacancy rate

An area with strong property demand is also more likely to attract tenants and own-stay occupiers to the same area.

One perspective to consider is to think about an area with a lot of units, it’ll be sensible to analyse and identify the vacancy rates in the development and also the surrounding area of the neighbourhood.

If the vacancy rate is high (for example, over 10%), be wary about the competition you may have, not just within the development you have invested in but also neighbouring developments.

In the instance of high vacancy, it is a tenant’s market to pick and choose.

In a competitive tenant-oriented market, you will need to consider ways to manage the vacancy or to attract tenants to pick your unit over others.

Before buying any property for investment, plan ahead for sufficient reserves to act as a buffer to sustain a higher vacancy period and/or putting in more capital to furnish the place or make your unit stand out among the competition.

3. Focus on mass market property and homes with a unique selling proposition

For property investment, consider buying mass-market product homes in the target area, but ensure that your entry price isn’t above similar transacted prices.

In the worst case scenario, purchasing a poorly selected property that has little valuation upside below the average transacted cost of similar properties in the area, at the very least, an investor would not be the first to lose money.

You should also look at the median property price of any one area.

You’ll often hear the saying “location location location”, however, the relevance to that mantra is not quite the same in this day and age.

More importantly, consider whether the price you are paying is around the average of the property market, whether or not the average Malaysian can afford to buy/or rent in the area that you’re targeting.

A typical rule of thumb we recommend is that a property investor invests at a price point within a 15% range of the median property for that particular area or development.

Our observation is that by limiting one’s scope to properties within this 15% price range, an investor is able to obtain an “above average” property that is more likely to represent good value for a future purchaser and prospective tenants.

To put it simply, a property within this price range maximizes represents a home the majority in that area is likely to afford to either rent or buy.

4. Be open to multiple rental strategies

Have an open mind and consider having multiple rental strategies for your property investment to target different rental prospect segments such as students, middle to high income locals, or expats so that you don’t just depend solely on one type of tenant.

For example, a “mass market property” in Bangsar, Mont Kiara, or TTDI isn’t within the same price bracket of a “mass market property” in Puchong, Selayang, Rawang or Sungai Buloh. This also applies to other hot areas within Malaysia.

A mass market development refers to properties that are priced and rented at affordable levels to the locals in that area. There are two parts to this equation:

Firstly, you must find out what the prices are for the various types of properties within an area. For example, segments condominiums landed bungalows and terrace houses to use as examples.

The second component is to roughly estimate who the locals in the area are and how much they’re likely to earn.

Typically, as a rule of thumb, a tenant or own stay would spend a maximum of one-third of their disposable income for housing expenses each month.

So if the usual rental price of a property is RM2,000 per month, the disposable income for that household should be around RM6,000 to RM8,000.

Do plan out multiple rental strategies like having a master tenant, rental on a per room basis, or even platforms like Airbnb, so that if one doesn’t work, you can try another approach.

If you buy a property relying on one stream of marketing, eg. only Airbnb, you run the risk of property management deciding to ban it.

And if your Airbnb unit isn’t profitable or requires too much time to manage or a black swan event like the Covid-19 pandemic leading to a lack of travellers, you’ll struggle with tenancy options.

5. Pay attention to the cash flow rule

Ideally, you’ll want a property investment where the minimum expected rent can cover 80% of your monthly mortgage instalment so that it wouldn’t deplete your cash flow to the point where you need to sacrifice your vacations, luxuries, cars and other basic necessities.

This also implies that with better cash flow, you could be eligible to obtain more loans in the future and therefore can invest in more properties or other assets of your choice.

Let’s use a subsale property that costs RM560,000 as a case study.

- Purchase Price = RM 560,000

- Loan Amount = RM 504,000

- 35 years tenure, 4.6% rate, Installment = RM2,416

Assumptions:

- There are no new major catalysts (e.g. transport infrastructure, central business district) that affect rental appreciation)

- There are similar developments that we can take as a comparison. Rental benchmarks are taken based on the transacted rental of units with a similar layout that’s less than 10 years old

Case A: If your rental = RM1,900

Rental-Installment Ratio = Rental / Installment = 1900 / 2416 = 78.6% → not qualify

Case B: If your rental = RM2,200

Rental-Installment Ratio = Rental / Installment = 2200 / 2416 = 91.1% → qualify

We can say that Case A is not good enough to be considered because the Rental Installment Ratio is below 80%.

Does this mean we disqualify Case A straight away? It depends.

We did the comparison based on assumptions that the area does not have any other major infrastructure to induce a more significant increase in the rental. Secondly, there are similar units in the area that aren’t much older than the subject.

Let’s look at another point of view, in which the scenario is that there are major infrastructure developments and amenities where the rental could possibly increase to RM2,000 for example:

Rental installment ratio = 2,000/ 2,416 = 82.7%

Therefore the property now should be taken into serious consideration.

OR

If there is no newer supply of similar units. Most existing developments are already more than 10 years old, and the rental benchmark against these developments aren’t apple-to-apple comparisons, and rent of RM1,900 would be an underestimation of rent potential.

New development with a modern facade and newer facilities has strong property investment potential and is in a strong position to command a higher rent.

Prospective tenants would likely be willing to pay a 10-20% premium to live in a more posh and modern residence, especially if they are expats in Malaysia.

These are just two examples of how one development becomes a “good” or “bad” development based on different factors.

6. Prioritise and achieve balance of rental yield and capital growth

Capital growth isn’t the only factor that makes property investment exciting; it’s also the fact that regular and constant income can be derived from real estate that makes it a sound investment choice for many investors.

Rental income is also a source of cash flow that can be used to pay down debt on the property. Rental yield, therefore, is simply the annualised rental income expressed as a percentage of the value of the property.

For example:

- Property value = RM400,000

- Monthly rental = RM2,000

- The annualised rental income = RM2,000 x 12 = RM24,000

- Rental yield calculated as a percentage = 24,000 / 400,000 = 6%

This is not only an important percentage as it helps to determine the return on investment so that the cash flow requirement of servicing and maintaining the property can be calculated, it also provides important information about the rate of capital growth.

A natural response would be to obtain as high a rental yield as possible. However, this may not always be the best route for the investor.

More often than not, an area experiencing high rental yield is more likely to have a lower capital growth, and vice versa.

Usually, when rental returns are high, investors are willing to accept a less than average capital growth rate. When rental yields are lower, investors must be compensated by achieving a higher than average capital growth rate.

Most people will strive to achieve a balance between making a bit more money now (higher rental yield, cash flow and lower capital growth rate) or more money later (lower rental yield, higher capital growth rate).

7. Calculate potential cash on cash return(COCR)

COCR can be used as a metric to quickly evaluate if you should pump in more capital for the investment property.

However, we urge caution when looking solely at this number as this figure may not necessarily be the most useful and accurate way to evaluate the rate of return beyond one year.

Cash on Cash Return = Income / Capital Outlay

Income = Rental income – (installments + maintenance + sinking + quit rent + fire insurance)

Capital outlay = Remodel/Reno + acquisition cost + progressive interest (if undercon)

Example :

To compare buying an undercon and subsale at nett price of RM550,000

a) Buying an undercon

- Price: RM611,000

- Loan amount : RM550,000

- Monthly installment = RM2,637

- Progressive interest costs: RM20,000

- Downpayment: ZERO

- Legal fee, stamp duty = Waived

- Renovation = RM25,000

- Capital outlay : RM 1,000 + RM 25,000 = RM 26,000

Assuming a first year rental of RM1,900 per month:

Income = (1,900×12) – (2,637+300) x 12 – 1,000 (assessment) = – RM13,444. In the first year, cash flow is negative for over RM13,000 and I spent RM26,000 to acquire the property

A quick calculation of COCR = -13,444 / 26,000 = -51.6%. This shows a negative COCR.

Consider the next investment option:

b) Buying a subsale

- Price: RM550,000

- Loan amount: RM495,000

- Monthly installment = RM2,373

- Progressive interest costs: ZERO

- Downpayment: RM55,000

- Legal fee, stamp duty, valuation = RM22,500

- Remodeling / Refurbishments = RM30,000

- Capital outlay: RM55,000 + RM22,500 + RM30,000 = RM107,500

Assuming a first year rental of RM2,200

Income = (2,200×12) – (2,373+300) x 12 – 1000 (assessment) = – RM6,676

In the first year, cash flow is at negative RM6,000 but I spent over RM100,000 to acquire the property

A quick calculation of COCR = -6,676 / 107,500 = -6.21%. This shows a negative COCR.

As COCR is only good in the short term, you need a better way to analyse your target property otherwise this number, which happens to be negative, will not tell you much. What can be deduced from this figure? Does a negative COCR tell you that you’re going to lose money?

Both options have negative COCR, but scenario (b) is less negative.

Scenario (a) capital outlay is RM26,000 with COCR -51.6% while scenario (b) capital outlay RM107,500, COCR -6.21%. How can you tell which one gives a better return? Can there be another way to evaluate these two options?

8. Meaningfully analyse your potential return on investment via internal rate of return (IRR)

As investors, it’s important to know the returns you make on your investment because you want to be able to know which are winning plays or losing plays.

For financial instruments like shares, bonds or unit trusts, keeping tabs on how well these investments are doing is quite easy because these investments have to produce some sort of “report card” each year; some may even produce it monthly.

If you don’t know how to check on the status of these investments, it’s probably best you engage a financial advisor to help you out.

However, it’s not that simple for property investments.

Using the internal rate of return (IRR) takes into consideration the cash outflows (your cost) of owning the property over any given investment horizon.

Cash on cash return (COCR) doesn’t give you an accurate picture of how good or bad your investments are, as you wouldn’t be able to make comparisons using COCR with the returns you get from other investments like entering into a business venture, Amanah Saham Bumiputera (ASB) funds, unit trusts, shares, or any other options available to you.

COCR = Annual cash flow / Total investment

Annual cash flow = all income – all expenses. It captures the snapshot year by year. If the COCR is positive, this suggests you’re getting some returns from the money put into this investment.

But what if the COCR is a negative number?

How would you benchmark against other asset classes? Property investment is a long term investment vehicle. Taking a snapshot return of any one particular year does not convey the full picture about whether you stand to make good or bad returns or lose money.

Rental yield = Annual rental / purchase price

This metric gives a quick indicator as to how the property is performing but it does not tell you anything about the expenses incurred to get the property rented out at a certain rental rate.

For example, let’s say owner A has two properties worth RM560,000 each of the same layout and size in the same development.

For one unit, the owner spends RM40,000 and he gets a rental of RM2,800 and for the other, he spends RM25,000 to get a rental of RM2,500.

Rental yield for unit #1 = 2800 x 12 / 560k = 6%

Rental yield for unit #2 = 2500 x 12 / 560k = 5.36%

The rental yield for unit #1 is 6% while unit #2 is 5.36%, but can we conclude that unit #1 is better than unit #2? It isn’t very accurate to make such an assumption just by looking at this equation.

If we restrict ourselves by analysing based just on rental yield, we will ignore the other extra cost of RM15,000 that it takes to be able to charge a RM300 premium on the rental yield of unit #1 compared to unit #2.

One way to address this cash flow is to use the internal rate of return as mentioned earlier. This is the third complimentary benchmarking tool to look at to help you make more informed decisions when evaluating a property, and is also useful for considering other asset investment classes.

IRR is simply the internal rate of return of the investment in which the net present value of all cash flow equals to zero.

When investing in property, it’s important for you to have a plan.

A plan is not the same as being told “let someone else pay your loan”; or “this property is yielding 20%” when you don’t know what those two sentences mean! Like all investments, there is a tried and tested method called IRR or internal rate of return.

Click here to learn more about internal rate of return and how to calculate it.

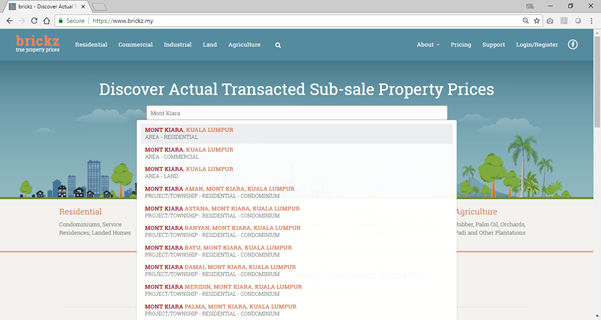

9. Evaluate based on transacted data

One of the worst methods of getting information to validate an investment is through forums or a non-expert.

While we recognise the advantage of getting tips or rumours if you’re going to be spending a lot of money on your investment, why take the risk at all?

To evaluate transacted data, begin by benchmarking the selling price of the target property against the transacted price of similar products in the area for the last 12 to 24 months.

Step 1: Go to https://www.brickz.my/

Step 2: Search for area or development name

Step 3: Search for area name

Step 4: Search for development name

10. Don’t forget your game plan

Building a portfolio is just like building up a football team – your team will require good cash flow properties (defensive) and good capital gains (offensive).

You can maintain your portfolio through defensive plays alone, but this strategy wouldn’t give you much cash to grow your portfolio.

The ability to consistently buy successful undercon properties involve many uncertainties that include the workmanship, delays or abandonment of the project, cancellation of nearby infrastructure and so on.

On the other hand, one can get more reliable data about transacted price and rental from subsales properties.

You can also visit the development and check out crucial factors like the profile of the residents and the upkeep of the development to entirely avoid the risk of construction delays or abandonment.

Cash from capital gain plays can be used for several purposes: loan reduction for defensive play properties, portfolio expansion, or used as self-rewards such as travelling, a dream car, or starting up a business.

Others may also use capital gains to fund children’s education or to keep for health emergencies.

You should also consider the time and effort of managing four units of low cost flats vs managing two residential properties for middle-upper income groups.

A low-cost only portfolio strategy does have its drawbacks.

Firstly, it’s more likely that you’ll encounter more issues managing lower income bracket tenants like late payments or even defaults.

Secondly, management spends on amenities improvements is limited. Most of these developments are run down and will not look appealing to future buyers or renters.

On the other hand, low-cost apartments provide better rental yields with limited capital appreciation.

Some people believe that buying landed properties gives better capital gain, sacrificing cash flow. Investing in too many landed developments will significantly affect short term cash flows compared to highrises.

In addition, to aim for better capital gains, people believe in investing in new areas or untested products (small units, new/low occupancy offices towers, landed play, negative cash flow) to hopefully enter at a lower price and exit the market after the boom, (for example, Setia Alam).

New areas and new mega developments involve huge resources and take time to build and there are a lot of dependencies and uncertainties involved.

Developers usually take a minimum of 10 years to build a self-sustaining township. Holding power and cash reserves are the most important considerations in deploying this strategy.

Your ability to maximise your property value depends on your holding power, your own patience, and cash reserves.

There are people who prefer the hybrid investment model (capital gain + cash flow), who would choose investments in high rises below market value while still offering decent cash flow.

And then there are others who use properties as a vehicle for wealth preservation or to provide a steady stream of income and tend to prioritise strong cash flow properties.

It all depends on your own resources in deploying proper investment planning, risk appetite, holding power, cashflow priorities and many factors.

The winning formula is about creating a balanced mix that suits your game plan to meet your financial goals. There are no free lunches out there so keep learning, and apply the knowledge learnt.

The more enlightened you get, you’ll make better, rational choices when building your nest egg for the future. All the best in your investment journey!

About the authors

Rozanna Rashid is a Licensed Financial Planner (CFP, IFP) and has an MSc in Real Estate Economics & Finance from the London School of Economics & Political Science. She can be contacted at rozanna@alpine-advisory.com

William Wong is an avid property investor and has an MBA (Finance) from Universiti Putra Malaysia. He is also the co-founder of Property Buddy PLT, a company that helps property investors strategise to achieve optimised rental returns via refurbishment for their investment properties